Euromonitor forecasts global inflation in the range of 6-9% in 2022, compared to an annual average of 3.8% in 2001-2019. Inflationary pressures have been rising since 2021, reaching a record level in many countries, and above central bank target rates in some advanced economies. Surging demand for goods, pandemic-induced disruptions, rising energy prices, and labour shortages have led to severe supply-demand mismatches. We expect inflationary pressures to remain high in most key economies, as some supply-demand mismatches and labour shortages could last throughout 2022, while the spillover effects of the war in Ukraine and economic sanctions on Russia have exacerbated this inflationary environment, particularly for energy and food prices.

Why inflation matters

Inflation represents the rate at which prices increase over time, based on a basket of consumer goods and services. Higher prices are driven by a combination of demand pull-factors (when demand for goods/services exceeds production capacity) and cost-push factors (when production costs increase prices).

Rising inflation has sparked business concerns about the potential impact on consumer spending, interest rates and corporate margins. It is vital for business to keep track of price dynamics and consumers’ changing behaviour amid an inflationary environment, as discretionary spending is squeezed, especially in lower-income segments or economies where a greater share of spending is on essential items.

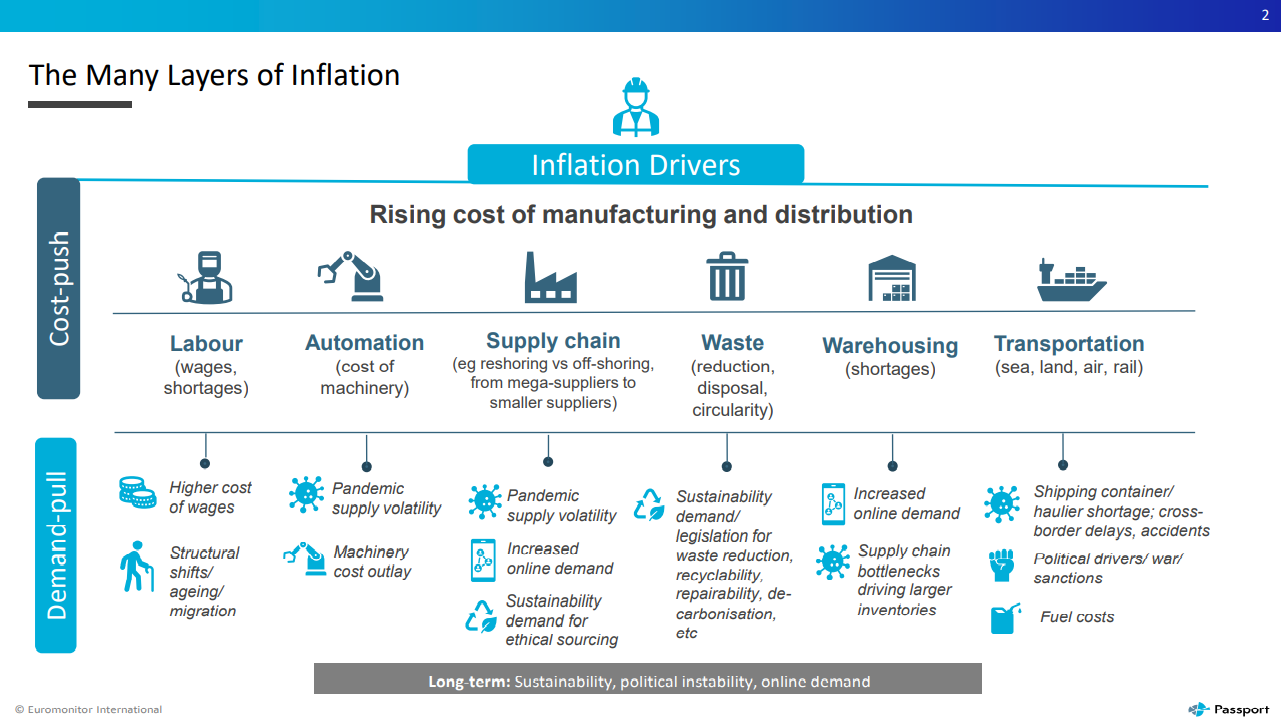

The different layers of inflation

Inflationary pressures felt across the globe have many layers, with costs increasing across a raft of areas from raw materials to distribution and manufacturing in between, themselves propelled by various demand-pull drivers such as the pandemic, increased online demand, political instability, climate change, sustainability regulation and shifts in demographics.

Rising cost of raw materials

- Prices of hard and soft commodities have been rising owing to pandemic-induced reduced supply chain issues (such as blocked ports, warehouse shortages/costs) and reduced production of specific commodities/ products (owing to ill workforces coupled with government-imposed lockdowns). This has been further exacerbated by political issues such as Brexit or war. The war in Ukraine and sanctions on Russia have precipitated price spikes in world oil prices along with those of commodities hitherto exported in large quantities by Ukraine as well as Russia such as steel, coal, barley, wheat, corn.

- Whilst sustainability tends to take a back seat when manufacturers are preoccupied with cost pressures elsewhere, it is still a driving force behind the demand for rPET and aluminium cans (both in short global supply), along with paper/carton as a sustainable packaging alternative to plastic, itself also helping service the boom for online sales. Whilst some cost-push factors, particularly those pandemic-induced issues are expected to level out longer term (future pandemics withstanding), some such as sustainability, climate change and scarcity of natural resource are expected to maintain prolonged pressures on prices.

Rising cost of manufacturing and distribution

- All aspects of the manufacturing chain, from labour to transportation have been impacted by the pandemic. Residual bottlenecks and shortages of all types of goods from machinery and spare parts to shipping containers and warehouse space, have propelled prices upwards. This has been further exacerbated by political instability in specific regions, which has spurred fuel costs, in turn impacting transportation channels. The ageing and movement of labour pools, along with increased costs of manual labour as well as its reverse, automation, have added to manufacturer costs, alongside the restricting of supply chains. Focus on near-/on-shoring has been prompted as much by sustainability demands on third party sourcing as by pandemic shortages, all incurring outlay costs.

- Sustainability regulation has also driven up costs of post-consumer waste in terms of extended producer responsibility, alongside repairability and recyclability mandates, something expected to continue exerting pressure well into the long-term. The mandated adoption of circular production methods is intended to diminish the demand and associated cost of raw materials and waste disposal over time, so could well have a dampening effect on the cost impact.

Company and consumer impact

- Companies have adopted several strategies over the past year to spread costs and pass some on to consumers without risking consumption decline. Pack size has become an ever more important area of pricing innovation for manufacturers of foods and beverages, as well as those of beauty and health and home care, amongst others. Common to them, as well as to manufacturers of electrical goods, are reductions in more expensive raw materials, components or ingredients. A reduction in SKU count is another strategy, thereby reducing the range and availability of goods available to consumers, whilst a reduction in number of price points for those SKUs remaining is another strategy, resulting in shifting price bands.

- Short-term, there is likely to be minimal change in consumer demand caused by an increase in prices as manufacturers adopt covert strategies. As the increase in the general cost of living starts to bite, downtrading is expected mid-term, with a prospect of overall consumption decline for a raft of industries, particularly discretionary goods, longer-term as volumes start to go down and value sales are kept afloat only by rising unit prices. Adding value to products via premiumising will help maintain sales in price bands designed to maintain value sales.